Understanding an Internal Control Framework

An internal control framework is the backbone of any organization’s financial integrity. It provides structure for how risks are managed, how reporting stays accurate, and how compliance is maintained. Every policy, approval, or review ties back to this foundation. Without it, financial reporting can become inconsistent and unreliable.

What is an internal control framework?

In practice, this framework connects the dots between business objectives and risk management. It keeps financial information dependable and audit-ready.

The five components of an internal control framework

A strong framework is made up of five parts, each reinforcing the others:

- Control environment: The tone set by leadership and company culture. It establishes expectations for integrity and accountability

- Risk assessment: The process of identifying and analyzing potential risks that could affect business goals.

- Control activities: The actual policies and procedures that make sure management directives are followed, such as reconciliations, approvals, or segregation of duties.

- Information and communication: How data flows across teams, ensuring people get the right information at the right time.

- Monitoring: Regular reviews and audits that check whether controls are working and highlight areas for improvement.

These elements together help maintain operational efficiency and reduce the likelihood of control breakdowns.

Why internal controls matter

Internal controls do more than satisfy compliance requirements. They make the difference between proactive risk management and reactive problem-solving.

With a well-structured framework, organizations gain:

- Accurate financial reporting, supported by clear documentation and review trails.

- Operational efficiency, as bottlenecks and duplicate work are reduced.

- Regulatory compliance, ensuring adherence to local and international standards.

- Improved governance, through consistent oversight and accountability.

When internal controls are weak or fragmented, the risk of financial misstatements, fraud, and compliance breaches increases. Strengthening these frameworks is essential for both accuracy and trust.

Implementing a control framework effectively

Rolling out or improving a control framework requires clear goals and consistent follow-through.

A practical implementation approach includes:

- Setting the right tone: Leadership needs to communicate the importance of internal controls.

- Assessing risks: Map out what could go wrong and prioritize those risks based on impact.

- Designing controls: Create clear, documented procedures that address those risks.

- Communicating roles: Make sure responsibilities and reporting lines are understood across teams.

- Monitoring performance: Regularly test and refine controls to keep them relevant as business processes evolve.

Automation can play a key role here, especially when audit and finance teams are stretched for time or working with large data volumes.

How automation strengthens internal controls

By automating repetitive steps like control testing, evidence cross-referencing, and sample documentation, teams reduce manual effort and minimize the risk of oversight.

Key capabilities that enhance internal controls include:

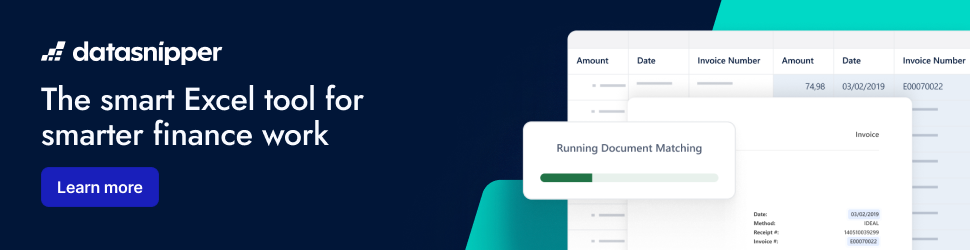

- Document Matching to reconcile data automatically and trace control results back to source evidence.

- Form and Invoice Extraction to capture and validate control data efficiently.

- Financial Statement Suite to check for consistency, accuracy, and version differences across financial reports.

- Tickmarks, comments, and Snips to document control testing results clearly and make reviews traceable.

- Company Templates to standardize internal control testing procedures across teams and entities.

Because DataSnipper is Excel-native, all control testing, sampling, and validation can be completed in one environment—reducing errors and improving collaboration across audit and finance teams.

What leading firms are achieving

Building a resilient control environment

Internal control frameworks are never static. They evolve as business models, regulations, and technologies change. Teams that combine strong control design with automation are better positioned to adapt quickly and maintain audit quality.

By working directly in Excel, DataSnipper helps internal audit and finance teams enhance documentation, improve review quality, and sustain compliance without rebuilding existing processes. The result is a control environment that’s accurate, auditable, and scalable.

.png?width=600&quality=70&format=auto&crop=16%3A9)